It’s All Coming Together

Stacking deals from Crusoe, Engine No1, Chevron, GE Vernova

𝗗𝗲𝗮𝗹𝘀 𝗮𝗻𝗻𝗼𝘂𝗻𝗰𝗲𝗱 𝗯𝘆 𝗖𝗿𝘂𝘀𝗼𝗲, 𝗘𝗻𝗴𝗶𝗻𝗲 𝗡𝗼𝟭, 𝗖𝗵𝗲𝘃𝗿𝗼𝗻, 𝗚𝗘 𝗩𝗲𝗿𝗻𝗼𝘃𝗮 𝗮𝗿𝗲 𝗺𝗮𝗸𝗶𝗻𝗴 𝗼𝗻𝗲 𝗼𝗳 𝘁𝗵𝗲 𝘄𝗶𝗻𝗻𝗶𝗻𝗴 𝗱𝗮𝘁𝗮 𝗰𝗲𝗻𝘁𝗲𝗿 𝗱𝗲𝘃𝗲𝗹𝗼𝗽𝗺𝗲𝗻𝘁 𝘀𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗲𝘀 𝘃𝗶𝘀𝗶𝗯𝗹𝗲.

And it is all about partnering to complete 𝙫𝙖𝙡𝙪𝙚 𝙘𝙝𝙖𝙞𝙣𝙨 𝙖𝙣𝙙 𝙩𝙝𝙚 𝙖𝙗𝙞𝙡𝙞𝙩𝙮 𝙩𝙝𝙚 𝙖𝙨𝙨𝙚𝙢𝙗𝙡𝙚, 𝙨𝙘𝙖𝙡𝙚 𝙖𝙣𝙙 𝙨𝙚𝙘𝙪𝙧𝙚 them.

What’s happened?

On January 28th Engine No. 1, Chevron and GE Vernova announced they were 𝗽𝗮𝗿𝘁𝗻𝗲𝗿𝗶𝗻𝗴 𝘁𝗼 𝗱𝗲𝘃𝗲𝗹𝗼𝗽 𝘂𝗽 𝘁𝗼 𝟰𝗚𝗪 𝗼𝗳 “𝗽𝗼𝘄𝗲𝗿 𝗳𝗼𝘂𝗻𝗱𝗿𝗶𝗲𝘀” based on gas-fired generation to support data center development.

What did that bring?

Chevron – a major gas producer with expertise in power, gas, and carbon capture.

Engine No. 1 – a capital provider with an investment focus on energy transformation.

GE Vernova – an equipment provider and accelerated access to 7HA natural gas turbines.

On March 17, Engine No. 1 and Crusoe—a company delivering AI-focused cloud computing infrastructure—announced a joint venture to create a "𝗿𝗲𝗮𝗹 𝗲𝘀𝘁𝗮𝘁𝗲 𝘀𝗼𝗹𝘂𝘁𝗶𝗼𝗻 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗔𝗜 𝗰𝗼𝗺𝗺𝘂𝗻𝗶𝘁𝘆" 𝘁𝗵𝗮𝘁 𝗱𝗶𝗿𝗲𝗰𝘁𝗹𝘆 𝗯𝗲𝗻𝗲𝗳𝗶𝘁𝘀 𝗳𝗿𝗼𝗺 𝗘𝗻𝗴𝗶𝗻𝗲 𝗡𝗼. 𝟭’𝘀 𝗲𝗮𝗿𝗹𝗶𝗲𝗿 𝗽𝗼𝘄𝗲𝗿 𝗽𝗮𝗿𝘁𝗻𝗲𝗿𝘀𝗵𝗶𝗽.

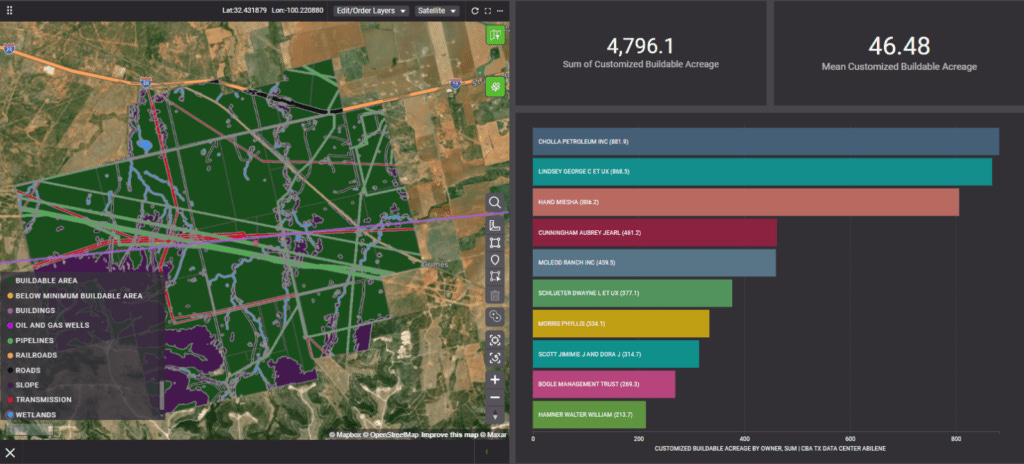

A glimpse of where they’re headed: Crusoe’s Lancium Clean Campus in Abilene, TX—set to scale up to 1.2GW—promises end-to-end solutions covering land acquisition, grid interconnects, renewables integration, and power orchestration.

Engine No. 1 first 𝘀𝗲𝗰𝘂𝗿𝗲𝗱 𝗽𝗼𝘄𝗲𝗿, 𝘁𝗵𝗲𝗻 𝗽𝗮𝗿𝘁𝗻𝗲𝗿𝗲𝗱 𝘄𝗶𝘁𝗵 𝗮 𝘀𝗰𝗮𝗹𝗮𝗯𝗹𝗲 𝗱𝗲𝘃𝗲𝗹𝗼𝗽𝗲𝗿 (Crusoe), and finally linked both into a complete data center solution. They assembled, scaled, and secured a value chain that is now market-ready—a compelling solution.

𝗪𝗵𝗲𝗿𝗲 𝗲𝗹𝘀𝗲 𝗶𝘀 𝘁𝗵𝗶𝘀 𝗵𝗮𝗽𝗽𝗲𝗻𝗶𝗻𝗴? 𝗜 𝗵𝗮𝘃𝗲 𝗮 𝗳𝗲𝘄 𝗶𝗱𝗲𝗮𝘀, 𝗯𝘂𝘁 𝗜’𝗱 𝗹𝗼𝘃𝗲 𝘁𝗼 𝗵𝗲𝗮𝗿 𝘄𝗵𝗮𝘁 𝘆𝗼𝘂’𝗿𝗲 𝘀𝗲𝗲𝗶𝗻𝗴.