Morning Energy is a syndicated note I publish through Enverus Intelligence. My contributions will also be distributed here. Please note that links frequently lead to content available only to subscribers of Enverus solutions. Please reach out if you have any questions. Thanks! - Ian.

The action in the Middle East has the world focused on energy supply. And for good reason. Hydrocarbon based energy price prices are racing higher. Crude prices are up 50% (hello $100 oil, we missed you) and LNG is up more than 80% (losing 10 Bcf/d from Qatar will do that). Even coal is up nearly 20% . US power, in contrast, looks like a model of tranquility. Henry Hub has barely moved and the weather forecasts look benign.

But don’t let the calm deceive you.

Something is happening to U.S. electricity demand. The peaks are teasing it. The shoulders are hiding it. Welcome to power’s masquerade ball.

The EIA confirmed last week that U.S. electricity generation hit a record 4,430 TWh in 2025 (NB: the linked EIA report erroneously states 4.43 TWh), up 2.8% from 2024, which itself was a prior record. After two decades of essentially flat generation, the obvious explanation is AI: hyperscalers building at a feverish pace and a grid straining under the weight of the digital economy. Compelling. But not the whole story.

Look at the load shape rather than the annual total. Our analysis of power demand against heating and cooling degree days finds that seasonal peaks last summer came in above weather-normalized expectations, but shoulder-season demand has been running below trend for the past couple of months (Figure 3). Those two signals together tell the story.

Data centers and electrification were strong enough to push summer peaks above where weather alone would put them. But in the shoulders, where data center load should also show up given its flat average profile, the signal has vanished, masked by something bigger.

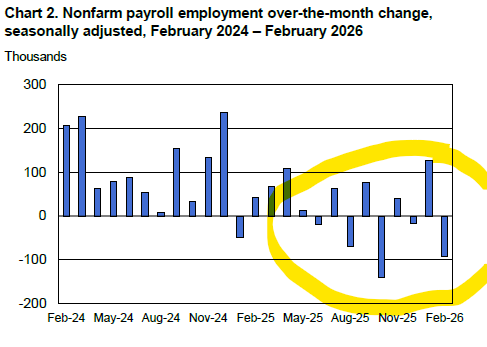

Friday’s jobs report may have spoiled the “Midnight Reveal”. Nonfarm payrolls fell by 92,000 in February, well below estimates, and the report shaved another 69,000 in downward revisions for January and December. A weakening economy may just have been the perfect mask for the emergent data center signal from the summer.

Emergent? Yes. Emergent. It is still early. Vistra’s CEO Jim Burke, whose company has contracted nearly 3.8 GW of nuclear capacity to hyperscalers and is actively building new gas capacity in West Texas, told investors last week that data centers will not meaningfully tighten supply and demand until late 2027 or early 2028. The (data center) guests are still arriving and when the economy finds its footing, the masks come off. That is when the power story will get interesting.

Comments, questions or things I missed? Send me a note (or hit reply) - I would love to hear from you. Thanks for reading!